Life Insurance: Your Shield Against Uncertainty

Life insurance is not just a policy; it’s a commitment to safeguarding your family’s financial future. While the topic nudges us to face our mortality, ensuring that our loved ones remain financially secure in our absence is paramount.

What is Life Insurance?

Life insurance is a contract between you and the insurance company. By paying regular premiums, the provider commits to offering a lump sum to your dependents after your demise. It’s a financial shield for your loved ones in dire scenarios.

Quick Facts About Life Insurance in Canada

- 22 million Canadians had an active life insurance policy in 2021, amounting to $5.3 trillion in coverage.

- The average life insurance coverage stood at $458,000 in 2021, a slight rise from 2020’s $442,000.

- Life insurance products paid out $14.3 billion in benefits in 2021, divided between death benefits ($8.8 billion) and living benefits ($5.5 billion).

Why is Life Insurance Important?

Life is filled with uncertainties. While we all wish for the best, preparing for the unexpected is vital. Life insurance is a financial safety net, ensuring your family’s financial stability in unforeseen circumstances. Here’s its pivotal role:

Financial Security

Life insurance acts as a financial pillar, enabling your family to manage significant expenses, from mortgage payments to utility bills, ensuring they continue to live comfortably.

Funeral Expenses

The emotional toll of losing a loved one is immense, and the added pressure of funeral expenses can be overwhelming. Life insurance steps in to shoulder these costs, allowing your family to focus on healing and remembrance.

Debt Management

In today’s world, debts are a common concern. Life insurance ensures that your family isn’t left grappling with these financial obligations, offering them a clear path to financial freedom.

Peace of Mind

Beyond the tangible benefits, life insurance offers emotional comfort. Knowing that your family will be financially secure, come what may, provides an unparalleled sense of peace and assurance.

What Does Life Insurance Cover?

Life insurance is more than just a policy; it’s a promise to protect your loved ones from financial hardships in the event of your passing. The death benefit, which is the sum your beneficiaries receive after your passing, is designed to address multiple financial challenges:

Mortgage

Life insurance can cover the remaining balance of your house payments, ensuring that your family retains their home without the burden of monthly mortgage payments.

Income Stream

If your family heavily relies on your income for their day-to-day expenses, life insurance can replace this income, ensuring they maintain their current lifestyle without financial disruptions.

Funeral Expenses

The costs associated with end-of-life ceremonies can be substantial. Life insurance ensures that these expenses are taken care of, allowing your family to grieve without the added stress of financial burdens..

Outstanding Debt

From credit card bills to personal loans, life insurance can assist in clearing any outstanding debts, ensuring your family isn’t left with financial liabilities.

School Tuition

Your dream of providing quality education for your children doesn’t have to end with you. Life insurance can fund their educational pursuits, ensuring they have the resources they need for a bright future.

Financial Gift

Beyond immediate needs, the death benefit can serve as a financial gift, allowing your loved ones to fulfill their dreams, invest, or even start a business.

Most Common Life Insurance Options in Canada

Navigating the world of life insurance can be daunting, given the myriad of options available. To simplify, let’s delve into the most prevalent life insurance types in Canada and their unique offerings.

Term Life Insurance

A straightforward and often affordable choice, term life insurance provides coverage for a predetermined period, be it 10, 20, or 30 years. It’s an ideal solution for those seeking protection during specific life stages, such as while raising a family or paying off a mortgage.

Whole Life Insurance

As the name suggests, whole life insurance offers lifelong coverage. Beyond just a death benefit, it often includes a cash value component, which can grow over time. This dual benefit – protection and savings – makes it a popular choice for many.

Universal Life Insurance

Merging the benefits of permanent coverage with investment opportunities, universal life insurance offers flexibility in premiums and potential growth in cash value. It’s tailored for those looking for both insurance protection and a savings avenue.

Term vs. Whole Life Insurance

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration of Coverage | Term life is designed to protect you for a specified duration, whether that’s five, ten, or thirty years. | Whole life offers continuous coverage, safeguarding you from the policy’s inception until your passing. |

| Purpose of Coverage | Ideal for those seeking protection during particular life phases, such as while a mortgage is active. | Suited for individuals with enduring coverage needs, like estate preservation. |

| Death Benefit | The benefit is a fixed amount and will be disbursed if you pass within the policy term. | The death benefit has the potential to appreciate over time and is assuredly paid upon your demise. |

| Policy Withdrawals | Term life doesn’t permit withdrawals during the policyholder’s lifetime. | Whole life typically allows withdrawals or loans against the accumulated cash value. |

| Affordability | Term life is often the more budget-friendly choice, given the potential that the policy might never pay out. | Whole life, with its guaranteed payout, generally comes with heftier premiums. |

| Cash Accumulation | Term policies don’t have a cash value component, meaning the death benefit remains static. | Whole life policies can amass cash value, offering you the flexibility to tap into funds and enhance the death benefit. |

Additional Life Insurance Products to Explore in Canada

Life insurance isn’t a one-size-fits-all solution. Depending on individual needs, there are specialized products available:

Critical Illness Insurance

Life is unpredictable, and critical illness insurance is there to offer a financial cushion if you’re diagnosed with a specified illness. It provides a lump-sum payment, allowing you to focus on recovery without financial stress.

Disability Insurance

In the event an injury or illness hinders your ability to work, disability insurance steps in. It offers a percentage of your income, ensuring you can manage your expenses during challenging times.

Mortgage Life Insurance

Tailored specifically for homeowners, this insurance ensures that your mortgage is paid off if something were to happen to you, providing peace of mind that your loved ones won’t be burdened with housing debts.

Funeral Insurance

End-of-life expenses can be substantial. Funeral insurance offers a dedicated coverage to manage these costs, allowing your family to commemorate your life without financial concerns.

Family Plan Insurance

Designed to offer coverage for the entire family under one policy, family plan insurance is a consolidated solution, ensuring every family member is protected.

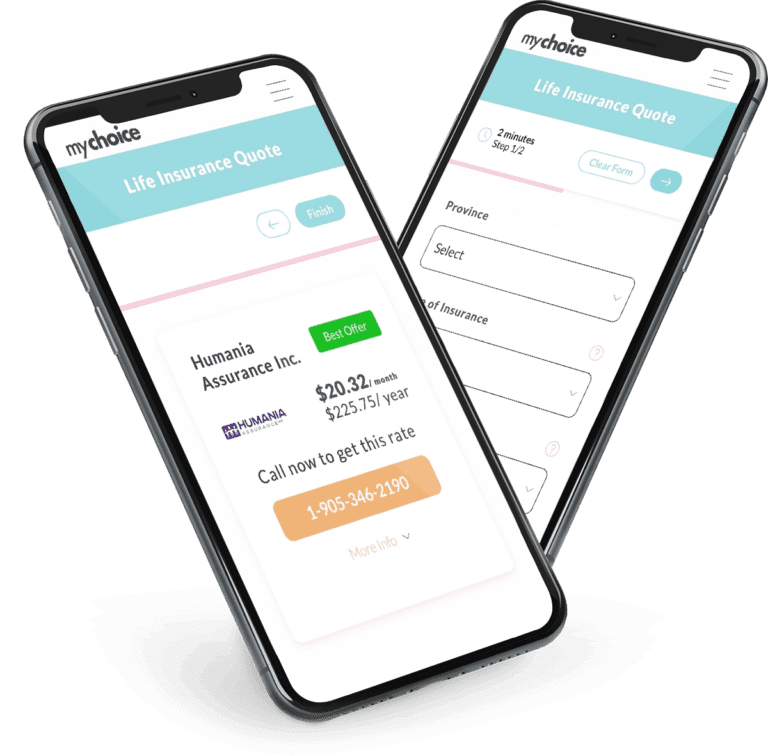

Unpacking Your Life Insurance Quote

Your life insurance quote isn’t plucked out of thin air. Insurers consider a myriad of personal factors to tailor your premium. Here’s a snapshot of some pivotal determinants:

Age

Naturally, as you age, the cost of insurance tends to rise. Some providers might even have age caps, post which they might not offer coverage.

Gender

On average, men might find themselves paying slightly more than women. This is rooted in statistical data suggesting that men might have a shorter life expectancy.

Health & Lifestyle Choices

Your health profile, including any pre-existing conditions or familial health history, plays a role. Lifestyle habits, like smoking or excessive alcohol consumption, can also influence premiums.

Type of Policy

Term life insurance, with its potential expiry, is often more wallet-friendly compared to permanent life insurance.

Duration of the Term

Shorter terms, like a 5-year policy, are typically cheaper than longer ones, such as a 30-year term, given the reduced likelihood of a claim.

Coverage Magnitude

It stands to reason that a more substantial death benefit would entail higher premiums. After all, greater protection has its price.

Life Insurance FAQs:

Who needs life insurance?

Anyone with financial dependents or obligations can benefit from life insurance. This includes parents, homeowners with mortgages, business owners, and individuals who want to ensure their loved ones are financially secure after their passing.

What is the difference between term life insurance and whole life insurance?

Term life insurance provides coverage for a specific duration, such as 10, 20, or 30 years. If the policyholder outlives the term, no benefit is paid out. Whole life insurance, on the other hand, offers lifelong coverage and includes a cash value component that can grow over time.

What is a life insurance beneficiary?

A beneficiary is an individual or entity designated by the policyholder to receive the death benefit from the life insurance policy upon the policyholder’s demise.

Can you get life insurance with pre-existing conditions?

Yes, many insurance providers offer policies to individuals with pre-existing conditions, though the premiums might be higher. It’s essential to disclose all health information during the application process to ensure the policy’s validity.

At what age should a person get life insurance?

It’s generally advisable to consider life insurance when one has financial dependents or obligations. However, securing a policy at a younger age can result in lower premiums due to the lower risk associated with youth.

How long does it take life insurance to pay out?

Once a claim is filed and all required documentation is provided, most insurance companies aim to process and pay out the death benefit within 30 to 60 days.

Is my life insurance policy comprehensively underwritten?

A fully underwritten policy involves a thorough assessment of the applicant’s health and lifestyle, ensuring accurate premium pricing based on the associated risks.

What constitutes a death benefit?

A death benefit is the sum paid out to the beneficiaries upon the insured’s death, as stipulated in the life insurance policy.

Will my life insurance premiums rise if my health deteriorates?

Once locked in, life insurance premiums typically remain constant. However, if you opt for a new policy or renewal, health changes might influence the rates.

What ensues if I die while my policy is in effect?

If the insured passes away during the active policy term, the designated beneficiaries receive the stipulated death benefit, provided all policy conditions are met.

Compare Life Insurance With Us Today

Life insurance is a pivotal financial instrument offering security and peace of mind. Whether you’re a budding professional, a parent, or nearing retirement, it’s an investment in your family’s future. At MyChoice, we’re dedicated to assisting you in finding the perfect policy tailored to your needs. Safeguard your loved ones and ensure their future remains bright.