Quote data from MyChoice.ca, March 2025

What Risks Affect Homeowners in Windsor?

Many things can cause home damage. Here are common risks to watch out for as a homeowner in Windsor:

Severe Event Probability in Windsor

Between August 28 and 30, 2017, Windsor recorded more than 200 mm of rain in two days, flooding thousands of basements and disrupting traffic.

Below are the MyChoice severe event probability scores for Windsor, based on the historical data from the Canadian Disaster Database collected since 1950. The percentages reflect the likelihood of a major event in question occurring at least once in the region in the next decade – relative to other regions and events.

How Much Does Home Insurance in Windsor Usually Cost?

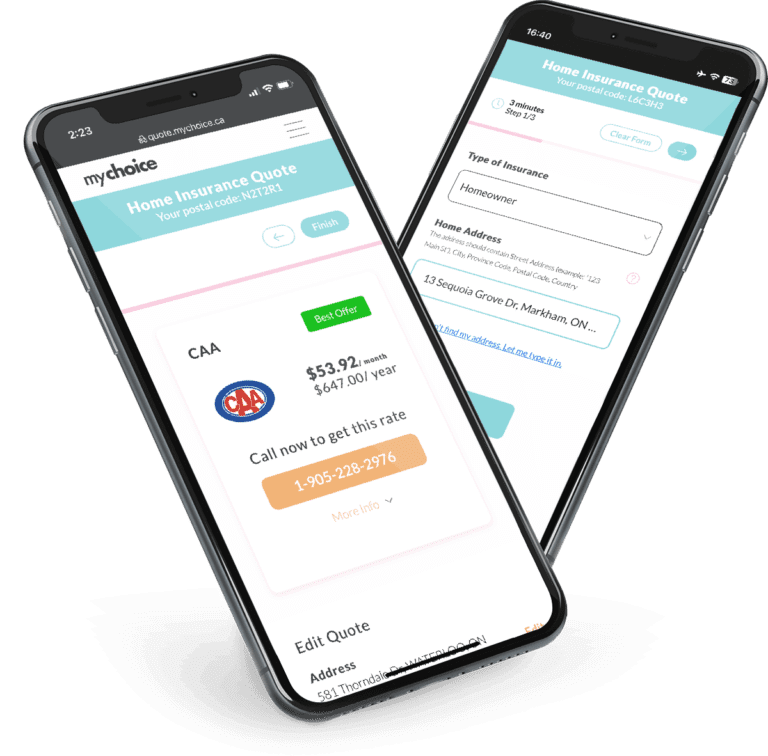

Home insurance in Windsor costs around $1,056 annually. Home insurance premiums are affected by factors like your home’s age, roofing type, proximity to fire hydrants, and more.

Using your home as a place of business may also influence your home insurance rates. Using your home for business means more people coming in and out of your property, increasing your liability and risk of losing belongings.

Quote data from MyChoice.ca, March 2025

Postal Codes With the Most Expensive Home Insurance in Windsor

L1S and L1N postal codes have above-average home insurance rates in Windsor.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| L1S | $1,055 |

| L1N | $1,097 |

Quote data from MyChoice.ca, March 2025

Postal Codes With the Least Expensive Home Insurance in Windsor

The L1T and L1Z postal codes have some of the cheapest home insurance rates in Windsor, since they have lower crime rates due to lower population density.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| L1T, L1Z | $1,004 |

Quote data from MyChoice.ca, March 2025

Housing Data in Windsor

Is living in Windsor right for you? Research can help you find the answer. Here’s a look at Windsor’s housing landscape based on the 2021 Census of Population to assist your research:

Homeownership Rate by Age in Windsor

Homeownership in Windsor is notably low among individuals aged 25 and younger, falling in line with the average ownership for city residents, like those who live in Windsor. As age increases we can see that the average homeownership rate does as well with roughly 69.5% residents aged between 40 and 75+ owning their home in Windsor.

| Age Group | Homeownership Rate |

|---|---|

| 15 to 24 | 15.4% |

| 25 to 39 | 47.5% |

| 40 to 54 | 63.8% |

| 55 to 74 | 69.8% |

| 75 and over | 75.4% |

Average Home Price in Windsor by Dwelling Type

Below are the average values of homes in Windsor, categorized by dwelling type:

| Type of Dwelling | Average Value |

|---|---|

| Detached | $576,000 |

| Semi-Detached | n/a |

| Freehold Townhouse | $665,000 |

Windsor Population Growth

Windsor’s population increased steadily from 217,188 to 229,660 people between 2016 and 2021. This indicates a growth rate of roughly 5.7% over these five years, underscoring Windsor’s steady progress as a city and its attraction for new residents.

This is by no means an exclusive list of risks typically excluded from a home insurance policy in Windsor. Talk to your home insurance provider to see what’s covered by your policy in case of loss or damage.

What Is Not Included in a Typical Home Insurance Policy?

Even if you’ve opted for a highly comprehensive home insurance policy, there are some risks that insurers explicitly don’t include as a covered peril. These are called “exclusions” by home insurers.

Here are the most common home insurance exclusions:

Why Do I Need Home Insurance in Windsor?

Home insurance isn’t legally required in Windsor. That said, having a policy is still a good idea. Home insurance protects you from unforeseen events that cause costly damages. Instead of paying to fix it out of pocket, your policy can lighten the financial load. Here’s a quick look at the reasons why you should get home insurance in Windsor:

FAQs About Home Insurance in Windsor

How can you get cheaper home insurance in Windsor?

If you’re trying to save money on your preferred home insurance coverage in Windsor, visit our Ontario page for practical tips.