Quote data from MyChoice.ca, March 2025

What Risks Affect Homeowners in Waterloo?

If you live in Waterloo, getting insurance can protect you against the following location-specific risks:

Severe Event Probability in Waterloo

On February 16, 2018, ice jams and unusually warm temperatures led to rising waters along the Grand River in Waterloo Region, damaging numerous houses.

Below are the MyChoice severe event probability scores for Waterloo, based on the historical data from the Canadian Disaster Database collected since 1950. The percentages reflect the likelihood of a major event in question occurring at least once in the region in the next decade – relative to other regions and events.

How Much Does Home Insurance in Waterloo Usually Cost?

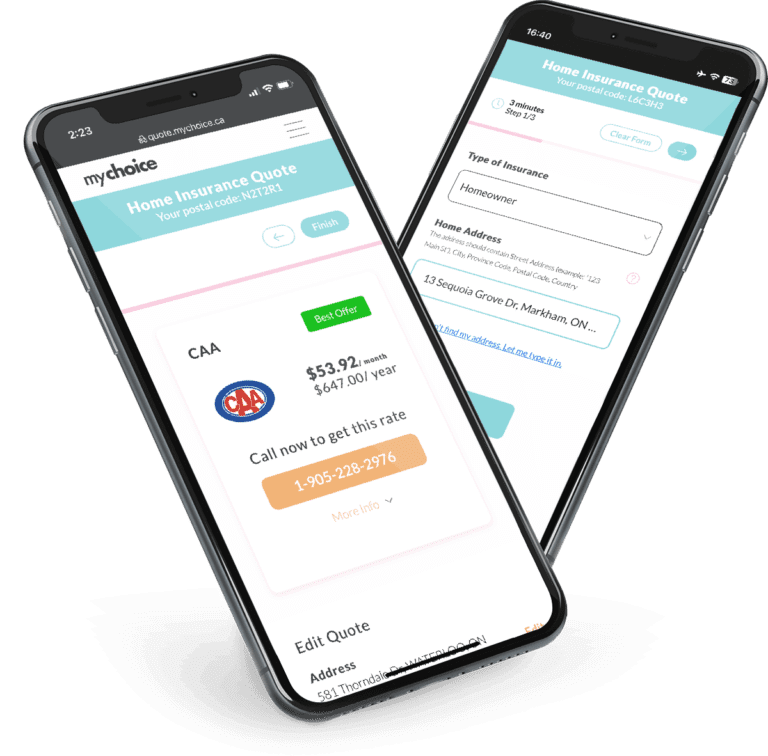

Home insurance in Waterloo usually costs around $1,304 annually. However, prices fluctuate depending on where in Waterloo you live and what coverage you need.

Quote data from MyChoice.ca, March 2025

Does Where You Live in Waterloo Affect Your Home Insurance?

Yes, where you live in Waterloo can affect your home insurance in the following ways:

Postal Codes With the Most Expensive Home Insurance in Waterloo

N2L and N2V postal codes have above-average home insurance rates in Waterloo.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| N2L | $1,367 |

| N2V | $1,409 |

Quote data from MyChoice.ca, March 2025

Postal Codes With the Least Expensive Home Insurance in Waterloo

Whereas the N2J postal code has some of the cheapest home insurance rates in Waterloo.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| N2J | $1,212 |

Quote data from MyChoice.ca, March 2025

Housing Data in Waterloo

Learn more about the housing landscape in Waterloo with this data from the 2021 Census of Population.

Homeownership Rate by Age in Waterloo

Homeownership in Waterloo is less than 50% for residents aged between 15 to 39, with only 41.8% of residents aged between 25 to 39 being a homeowner. This average increases to around 75% for all residents aged between 40 to 75+. Highlighting a strong rental market for the younger residents of the city.

| Age Group | Homeownership Rate |

|---|---|

| 15 to 24 | 10.8% |

| 25 to 39 | 41.8% |

| 40 to 54 | 73.8% |

| 55 to 74 | 79.7% |

| 75 and over | 72.4% |

Average Home Price in Waterloo by Dwelling Type

Below are the average values of homes in Waterloo, categorized by dwelling type:

| Type of Dwelling | Average Value |

|---|---|

| Detached | $955,000 |

| Semi-Detached | $645,000 |

| Freehold Townhouse | $647,950 |

Waterloo Population Growth

Waterloo’s population increased quite rapidly from 104,986 to 121,436 people between 2016 and 2021. This indicates a growth rate of roughly 15.6% over the course of the five years, underscoring Waterloo’s appeal for newcomers to the city.

What Is Not Included in a Typical Home Insurance Policy?

Even if you’ve opted for a highly comprehensive home insurance policy, there are some risks that insurers explicitly don’t include as a covered peril. These are called “exclusions” by home insurers.

Here are the most common home insurance exclusions:

This is by no means an exclusive list of risks typically excluded from a home insurance policy in Waterloo. Talk to your home insurance provider to see what’s covered by your policy in case of loss or damage.

Why Do I Need Home Insurance in Waterloo?

Purchasing a property in Waterloo is expensive, so while you don’t need home insurance, protecting it with the right policy is a significant financial advantage. Here are a few reasons getting home insurance for your Waterloo home is a good idea:

- You get financial protection if your home is impacted by natural disasters, vandalism, and theft.

- You get financial protection if someone gets injured in your home and files a lawsuit against you.

- If your home becomes uninhabitable, you get financial assistance for temporary accommodations, meals, and other necessities.

- You can satisfy mortgage requirements.

- You get peace of mind.

How Can I Get Cheap Home Insurance in Waterloo?

If you’re trying to save money on your preferred home insurance coverage in Waterloo, visit our Ontario page for practical tips.