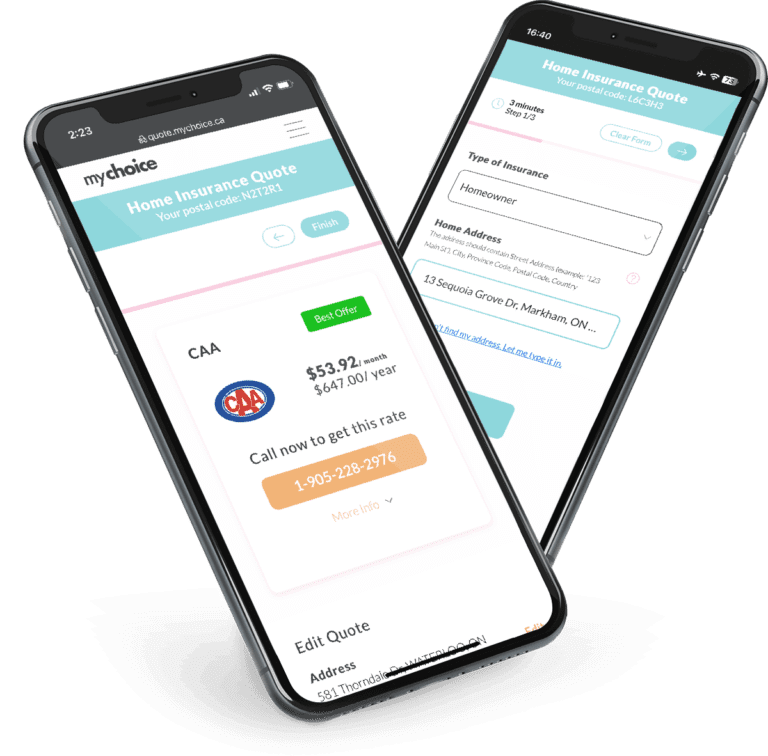

Quote data from MyChoice.ca, March 2025

What Risks Affect Homeowners in Toronto?

Many homeowners in Canada are affected by similar risks. However, there are some specific risks which Toronto homeowners should keep an eye on, and these are:

This is by no means an exclusive list of risks typically excluded from a home insurance policy in Toronto. Talk to your home insurance provider to see what’s covered by your policy in case of loss or damage.

Severe Event Probability in Toronto

On July 8, 2013, Toronto faced one of its worst flooding events as 126 mm of rain fell in a matter of hours, knocking out power for 300,000 people.

Below are the MyChoice severe event probability scores for Toronto, based on the historical data from the Canadian Disaster Database collected since 1950. The percentages reflect the likelihood of a major event in question occurring at least once in the region in the next decade – relative to other regions and events.

How Much Does Home Insurance in Toronto Usually Cost?

It’s hard to give a definitive answer to the typical cost of home insurance in Toronto, as your quotes are affected by factors like your home’s age and value, your policy type, and your location. The cost also differs between home insurance companies as each one has different methods for assessing risks and costs of coverage. This is why premiums differ between providers.

Expect to pay a premium within a range of $1,039 to $2,079 annually for Toronto home insurance. On average, Toronto home insurance costs $1,593 annually, which is higher than the average Ontario home insurance rate.

Quote data from MyChoice.ca, March 2025

Does Where You Live in Toronto Affect Your Home Insurance?

Yes, where you live in Toronto affects your home insurance. Certain areas pose higher risks for different perils and natural disasters, leading to increased chances of filing claims. As a result, different areas may have varying home insurance quotes for homes of similar size, value, and condition.

For example, Toronto’s Danforth-Greektown area is known as one of the city’s safer and more family-friendly neighbourhoods, so a home insurer may consider it less likely that you’ll file a claim. On the other hand, living in bustling Moss Park near the Downtown Core may get you higher quotes because of its historically high property crime rates. Living in densely populated neighbourhoods like Queens Quay and King West may raise concerns for your insurer about the risk of spreading fires in clustered homes.

Compare quotes using MyChoice to see how much home insurance costs in your Toronto neighbourhood. This will help you find the most competitive quotes for your area so you can find the best deal no matter where you live.

Postal Codes With the Most Expensive Home Insurance in Toronto

M4N and M6E postal codes have above-average home insurance rates in Toronto.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| M4N | $1,678 |

| M6E | $1,651 |

Quote data from MyChoice.ca, March 2025

Postal Codes With the Least Expensive Home Insurance in Toronto

The M6K and M6J postal codes have some of the cheapest home insurance rates in Toronto.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| M6K, M6J | $1,495 |

Quote data from MyChoice.ca, March 2025

Why Are Toronto Home Insurance Rates so Expensive?

There are three factors that may be driving up Toronto home insurance rates. Here’s a quick explanation of why these things make premiums higher in Toronto:

- Greater number of older properties: Most homes in Toronto are quite old, so it’s more likely that they have older systems for heating, plumbing, and electricity. This increases your likelihood of filing a claim for a fire or flood.

- Higher real estate values: Real estate prices indirectly affect home insurance premiums. As home values go up, so do the cost of rebuilding and the amount of coverage you’ll need from a policy.

- Housing density: Toronto is densely populated, and most of its homes are connected houses or apartments with very little space between units. This increases the risk of spreading fires between homes.

Housing Data in Toronto

Curious about the average Toronto home’s age, condition, and type? Here’s a simple overview of Toronto housing based on the 2021 Census of Population:

Homeownership Rate by Age in Toronto

Homeownership in Toronto is unsurprisingly less than in other cities in Ontario, this is largely due to the higher-than-average real estate costs in the city, making it harder for younger residents to obtain homeownership. Interestingly only around half of residents aged between 40 and 54 are homeowners, this average increases slightly to 65.5% for residents 55 or older.

| Age Group | Homeownership Rate |

|---|---|

| 15 to 24 | 19.5% |

| 25 to 39 | 33.8% |

| 40 to 54 | 53.6% |

| 55 to 74 | 62.6% |

| 75 and over | 68.9% |

Average Home Price in Toronto by Dwelling Type

Below are the average values of homes in Toronto, categorized by dwelling type:

| Type of Dwelling | Average Value |

|---|---|

| Detached | $1,617,500 |

| Semi-Detached | $1,360,000 |

| Freehold Townhouse | $1,344,500 |

Toronto Population Growth

Toronto’s population continued to increase from 2,731,571 to 2,794,356 people between 2016 and 2021, indicating a growth rate of roughly 2.29% over the specified five years.

What Is Not Included in a Typical Home Insurance Policy?

Even if you’ve opted for a highly comprehensive home insurance policy, there are some risks that insurers explicitly don’t include as a covered peril. These are called “exclusions” by home insurers.

Here are the most common home insurance exclusions:

Why Do I Need Home Insurance in Toronto?

Home insurance isn’t mandatory in Toronto. However, it’s strongly encouraged that you get a policy because of these reasons:

How Can I Get Cheap Home Insurance in Toronto?

If you’re trying to save money on your preferred home insurance coverage in Toronto, visit our Ontario page for practical tips.