Quote data from MyChoice.ca, March 2025

What Risks Affect Homeowners in Scarborough?

Like any Ontario city, Scarborough comes with several risks to homeowners. These potential threats include the following:

Severe Event Probability in Scarborough

On July 8, 2013, torrential rainfall saturated Scarborough’s streets and caused widespread closures as the city struggled with flash floods.

Below are the MyChoice severe event probability scores for Scarborough, based on the historical data from the Canadian Disaster Database collected since 1950. The percentages reflect the likelihood of a major event in question occurring at least once in the region in the next decade – relative to other regions and events.

How Much Does Home Insurance in Scarborough Usually Cost?

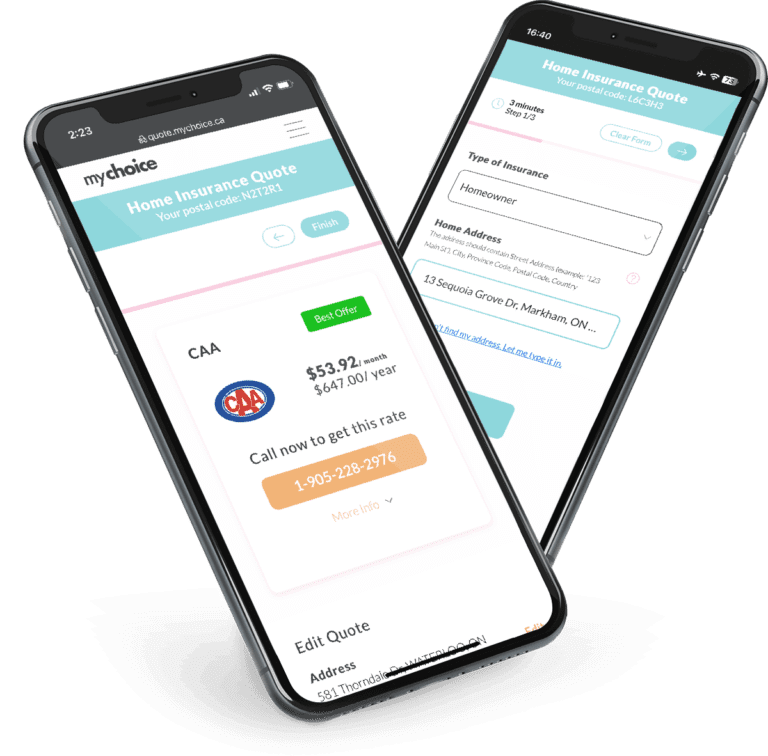

The average cost of home insurance in Scarborough is $1,010 However, prices may fluctuate depending on which Scarborough neighbourhood you have a property in.

Quote data from MyChoice.ca, March 2025

Does Where You Live in Scarborough Affect Your Home Insurance?

Yes, where you live in Scarborough can influence your home insurance rates. Here are a few factors that can impact your final policy rates:

Postal Codes With the Most Expensive Home Insurance in Scarborough

M1C tends to have homes with above-average home insurance rates in Scarborough.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| M1C | $1,159 |

| M1E | $1,107 |

Quote data from MyChoice.ca, March 2025

Postal Codes With the Least Expensive Home Insurance in Scarborough

The M1B and M1E postal codes have some of the cheapest home insurance rates in Scarborough.

| Postal Code | Average Annual Home Insurance Premium |

|---|---|

| M1B | $1,004 |

Quote data from MyChoice.ca, March 2025

Housing Data in Scarborough

To get a better picture of the housing landscape in Scarborough, review the following housing data from the 2021 Census of Population.

Average Home Price in Scarborough by Dwelling Type

Below are the average values of homes in Scarborough, categorized by dwelling type:

| Type of Dwelling | Average Value |

|---|---|

| Detached | $1,152,000 |

| Semi-Detached | $975,000 |

| Freehold Townhouse | $933,500 |

Scarborough Population Growth

Scarborough’s population slightly increased from 102,386 to 103,449 people between 2016 and 2021, indicating a growth rate of roughly 1% over the course of the five years.

What Is Not Included in a Typical Home Insurance Policy?

Even if you’ve opted for a highly comprehensive home insurance policy, there are some risks that insurers explicitly don’t include as a covered peril. These are called “exclusions” by home insurers.

Here are the most common home insurance exclusions:

This is by no means an exclusive list of risks typically excluded from a home insurance policy in Scarborough. Talk to your home insurance provider to see what’s covered by your policy in case of loss or damage.

Why Do I Need Home Insurance in Scarborough?

While not mandated, there are many reasons why getting home insurance in Scarborough is a good idea. These include the following:

- To provide financial protection for personal liability, in case someone is injured on your property

- To rebuild your home in case of perils like fires, vandalism, storm damage, falling objects, and explosions

- To replace your personal belongings in case of loss

- To provide financial assistance in case your home becomes uninhabitable for any reason

- To meet mortgage requirements

- To provide yourself with peace of mind

How You Can Get Cheap Home Insurance in Scarborough

If you’re trying to save money on your preferred home insurance coverage in Scarborough, visit our Ontario page for practical tips.