Quote data from MyChoice.ca, March 2025

What Risks Affect Homeowners in Edmonton

Edmonton is often exposed to extreme weather. Here are some common risk factors homeowners in Edmonton should watch out for:

Severe Event Probability in Edmonton

On July 31, 1987, Edmonton suffered its deadliest tornado on record, killing 27 people, injuring 600, and leaving about 1,700 homeless.

Below are the MyChoice severe event probability scores for Edmonton, based on the historical data from the Canadian Disaster Database collected since 1950. The percentages reflect the likelihood of a major event in question occurring at least once in the region in the next decade – relative to other regions and events.

How Much Does Home Insurance in Edmonton Usually Cost?

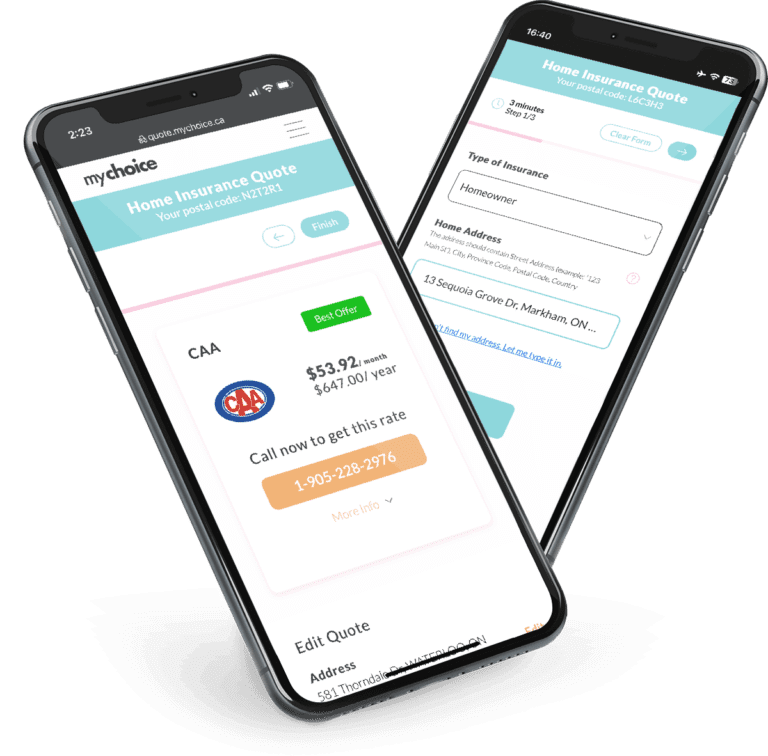

Home insurance in Edmonton costs around $925 annually. Home insurance premiums are affected by factors like your home’s age, roofing type, proximity to fire hydrants, and more.

Using your home as a place of business may also influence your home insurance rates. Using your home for business means more people coming in and out of your property, increasing your liability and risk of losing belongings.

Quote data from MyChoice.ca, March 2025

Housing Data in Edmonton

Edmonton has been widely known as the oil capital of Canada since the 1940s thanks to its prevalent petrochemical industry presence. Naturally, you’ll find lots of work in the energy sector. However, Edmonton also has a very diverse economy, including strong healthcare and manufacturing sectors. All of these industries are backed up by a powerful technology industry, which means Edmonton residents have lots of career opportunities.

Edmonton is an immigrant hub, boasting 4% of the country’s immigrant population. The cultural diversity means Edmonton residents will see a lot of new cultural experiences from around the globe. One of its biggest cultural events is the Edmonton International Fringe Festival, the second-largest arts festival of its kind in the world.

The average household income in Edmonton is $10,000 over the national average. What makes it better is that the city’s average living cost is 9% below the national average. That means you make more money and live more affordably if you call Edmonton home.

Researching a city’s housing landscape is a good way to see whether living there is right for you. Here’s a detailed look at some key residential statistics in Edmonton from the 2021 Census of Population:

Homeownership Rate by Age in Edmonton

The homeownership rate is quite high in Edmonton among people aged 55 and older, while only two in four young adults (25-39) own a house.

| Age Group | Homeownership Rate |

|---|---|

| 15 to 24 | 12.9% |

| 25 to 39 | 51.3% |

| 40 to 54 | 68.4% |

| 55 to 74 | 74.5% |

| 75 and over | 76.3% |

Average Home Price in Edmonton by Dwelling Type

Below are the average values of homes in Edmonton, categorized by dwelling type:

| Type of Dwelling | Average Value |

|---|---|

| Detached | $495,500 |

| Semi-Detached | $400,000 |

| Freehold Townhouse | $250,000 |

Edmonton Population Growth

Edmonton’s population grew 8.33% between the years of 2016 and 2021.

What Is Not Included in a Typical Home Insurance Policy?

Even if you’ve opted for a highly comprehensive home insurance policy, there are some risks that insurers explicitly don’t include as a covered peril. These are called “exclusions” by home insurers.

Here are the most common home insurance exclusions:

This is by no means an exclusive list of risks typically excluded from a home insurance policy in Edmonton. Talk to your home insurance provider to see what’s covered by your policy in case of loss or damage.

Why Do I Need Home Insurance in Edmonton?

There are many risks to your Edmonton home. From flooding due to heavy rain to fires, unforeseen incidents can damage your home or its attached structures severely, which can take a lot of money to repair. Somebody can even get into an accident on your property, which might result in hefty legal and medical fees.

Unexpected expenses due to these incidents can stretch your finances thin. The good news is that home insurance can help. A home insurance policy can foot your home repair bills if a covered peril damages it. Additionally, it pays for the many costs associated with personal injury lawsuits.

With the many options for home insurance, which one is right for you? There’s no one “best” home insurance policy for everybody, so you need to learn more about home insurance in Edmonton to make the right decisions.

You technically don’t need home insurance in Edmonton, because it’s not a legal requirement for homeowners. However, you should still get a policy to protect your home as well as its contents. Here are three main reasons why having a home insurance policy is a good idea:

How You Can Get Cheap Home Insurance in Edmonton

Visit our main provincial page to view the list of practical tips on how to get cheaper home insurance.