Vacationing at your cottage in Canada is a great way to spend your holidays, whether its summer or winter, it’s a welcome break from the hustle and bustle of your everyday life and provides time for you to create lasting memories with your loved ones.

Just like your home, your cottage needs insurance protection. Insurance is even more important since you’re likely leaving your holiday home vacant for most of the year. Knowing that insurance covers your holiday home even when it’s damaged while you’re away will give you peace of mind.

What is Cottage and Seasonal Property Insurance?

Cottage and seasonal property insurance in Canada refers to insurance protection that covers homes that aren’t your primary residence. For Canadians, the most common vacation properties include cottages and ski chalets.

Generally, cottage insurance provides many of the same coverage options that home insurance does. A typical cottage insurance policy would contain property, contents, and liability coverage.

How Much Does Cottage Insurance Usually Cost?

Cottage insurance generally costs between $800 and $3,000 annually. Like home insurance, your premiums are calculated according to various factors related to your holiday home, like its size, features, amenities, and location.

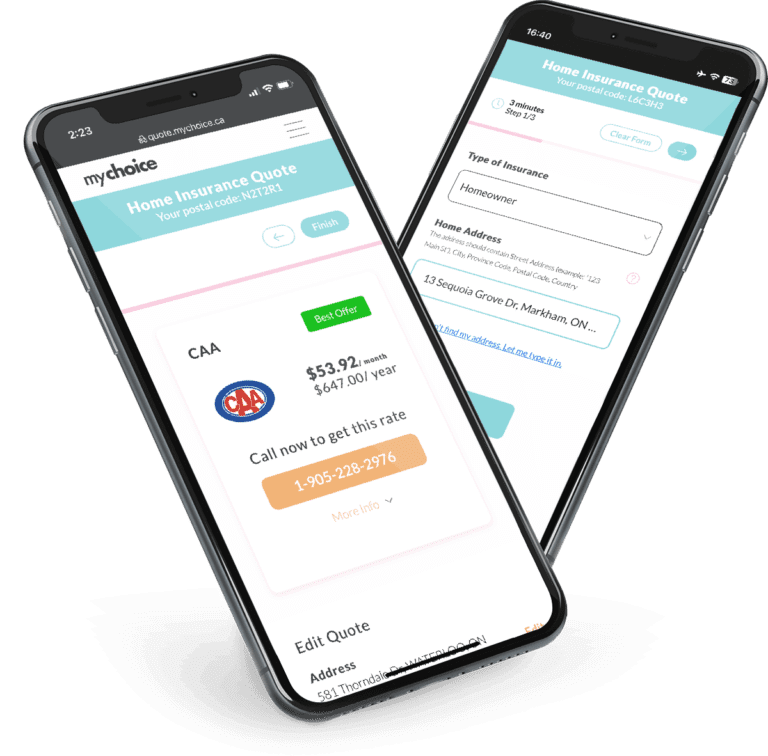

A good way to get the best cottage insurance deals is by comparing options from multiple insurance companies, another good approach would be to bundle it with your regular home insurance. My Choice can help you explore and compare deals from Canada’s top insurance companies to ensure you get the best protection for your budget.

What Risks Does Cottage Insurance Typically Cover?

Cottage insurance typically protects you from perils like fire, theft, and severe weather. However, your cottage insurance coverage details will depend on what kind of insurance you purchase. The two common types of cottage insurance are:

Here’s a list of common risks that are covered by cottage insurance:

- Property damage from fire, water, severe weather, and vandalism

- Theft

- Third-party liabilities

- Damage to outbuildings and landscaping

What’s covered and not covered may vary between insurers, so ask your broker about your cottage insurance coverage details.

What Risks Are Not Covered by Cottage Insurance?

Examples of risks not covered by cottage insurance include earthquakes, intentional damage, and mechanical breakdowns.

Here’s a list of risks that aren’t typically covered by cottage insurance:

- Vermin and wildlife damage

- Sewer backup

- Mechanical breakdowns

- Intentional damage

- Earthquakes

- Property wear and tear

- Risks with over two claims within the past three years

- Terrorism and war

- Other people’s belongings

Fortunately, you can get protection from some of these risks by purchasing additional coverage.

How Is Cottage Insurance Different From Home Insurance?

Cottage insurance differs from home insurance because it’s tailored to protect your holiday property from unforeseen incidents in remote locations, where cottages are often located.

Insurers calculate risk for cottage insurance differently because holiday homes aren’t usually occupied year-round, and access to emergency services may be limited due to their remote locations. Because they’re often unoccupied and far away from major population centres, cottages are often at higher risk of thefts, vandalism, and fires.

Essentially, getting cottage insurance tends to be a little trickier and costlier because more risks are involved than regular home insurance.

Some Common Claims for Cottage Insurance

Most claims for cottage insurance are similar to home insurance claims. Water damage, fires, and theft are some of the more common cottage insurance claims you’ll find. Let’s take a look at examples of common cottage insurance claims and how you can mitigate the risk:

Commonly Asked Questions About Cottage Insurance

Is cottage insurance cheaper than home insurance in Canada?

Cottage insurance generally isn’t cheaper than home insurance in Canada. Insuring holiday properties is more expensive because cottages tend to be more remote, which means access to emergency services is harder. The remote location of most cottages also makes reconstruction efforts harder and costlier. However, if you were able to bundle your cottage insurance with some other insurance product you have then you may be able to get a cheaper overall rate.

Does cottage insurance apply if I rent it out?

Cottage insurance doesn’t apply if you rent it out because your cottage is under commercial use during that time. You need rental cottage insurance if you want to protect your cottage while renting it out.

Can I bundle my cottage or cabin insurance with my home insurance?

Yes, you can bundle cottage or cabin insurance with home insurance. Ask your insurance broker or agent about how you can do so.

Do I need to tell my insurance broker that I rent my cottage?

Yes, you must tell your insurance broker you rent your cottage. If you don’t tell your insurer that you rented your cottage, they may deny your insurance claim or drop you as a customer altogether.

What insurance do I need if I rent my cottage?

If you rent out your cottage, you’ll need a rental property insurance policy. Your regular cottage insurance policy won’t be enough because renting your cottage out means you’re putting it to commercial use.

Should I have contents insurance for my cottage?

You should have contents insurance for your cottage, but most cottage insurance policies already have it as part of your coverage.

Does cottage insurance cover me from damage caused by a bear?

Some cottage insurance policies may cover you from damage caused by bears. Check your policy’s details if you’re eligible for bear damage coverage. If not, ask your insurer to purchase additional bear damage protection.

What type of buildings does cottage insurance apply to?

Cottage insurance applies to various types of buildings that are considered vacation properties.

Examples include:

– Cottages

– Island cottages

– Lake houses

– Ski chalets

– Lodges

– Cabins

What other cottage risks are worth insuring?

Some cottage risks that are worth insuring or getting extra protection for are:

– Cottage contents damage or loss

– Dock or boathouse damage

– Water damage that’s not covered in your main policy

– Vermin and animal damage