What Are Demerit Points?

Demerit points are added to your licence if you’re convicted or found guilty of specific driving violations under the Ontario Highway Traffic Act, such as speeding, careless or distracted driving, or failing to obey road signs. This can range from two points for relatively minor infractions to seven points for severe violations.

Every driver starts with zero points and can face severe penalties if they accumulate too many. The threshold for these penalties depends on the type of licence you have (i.e., 15 for experienced drivers, nine for novice drivers).

Aside from Ontario, you can also accumulate demerit points if you break traffic laws in other Canadian provinces and territories, as well as the states of New York and Michigan.

How Long Do Demerit Points Stay On Your Record?

Demerit points stay on your record for two years from the offence date, not the conviction date. This is typically the date you paid the traffic ticket or the date of conviction (if you went through a trial). Because court hearings can take a while, court proceedings may delay the conviction date, but the two-year demerit period still begins on the offence date.

That said, convictions and collisions can stay on your record for longer, potentially affecting your insurance rates for up to five years.

How to Check Your Demerit Points in Ontario

As your demerits aren’t always listed on the traffic ticket, you should regularly check your driving record to see how many points you’ve accumulated. You can request a driver’s abstract by mail, in person, or online via the Service Ontario website.

The fees for these records are as follows:

| Record | Certification | ETD | Cost |

|---|---|---|---|

| 3-year record | Uncertified | Immediate | $12 |

| Certified | 15 business days | $18 | |

| 5-year record | Uncertified | 15 business days | $12 |

| Certified | 15 business days | $18 | |

| Complete driver record | Uncertified | 6-8 weeks | $48 |

| Certified | 6-8 weeks | $54 |

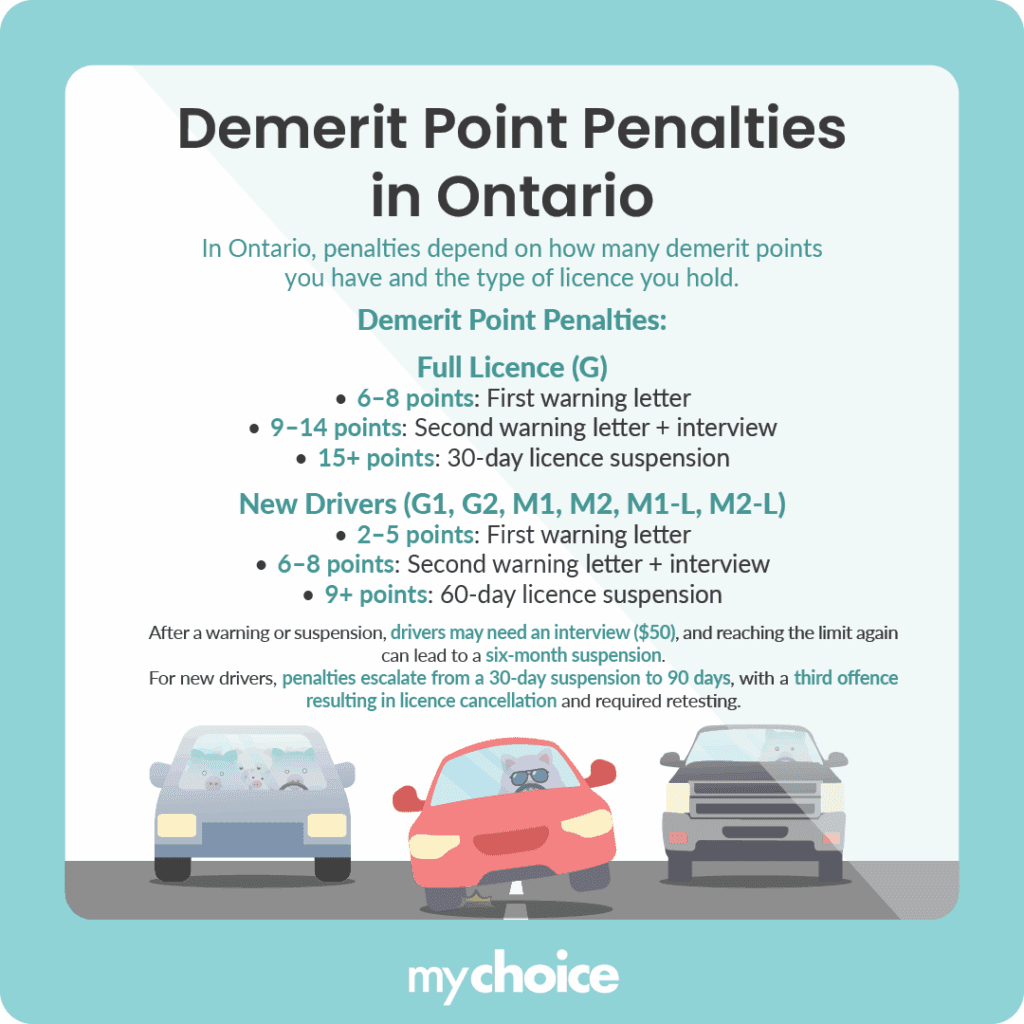

Penalties for Demerit Points

There are consequences to accumulating too many demerit points, depending on how many are on your record and what kind of licence you have.

Below are the penalties for drivers with full licences and new drivers (i.e., drivers with G1, G2, M1, M2, M1-L, and M2-L licences):

| Full Licence (G) | New Drivers (G1, G2, M1, M2, M1-L, M2-L) | ||

| Points | Penalty for Full Licence | Points | Penalty |

| 6-8 | First warning letter | 2-5 | First warning letter |

| 9-14 | Second warning letter + interview | 6-8 | Second warning letter + interview |

| 15+ | Licence suspension for 30 days | 9+ | Licence suspension for 60 days |

Below is a detailed explanation of each consequence you will face in case of demerit point accumulation.

How Speeding Affects Demerit Points in Ontario

The number of points applied to your driving record is based on the severity of the infraction. For example, here are the demerit points you can get depending on how much you’ve exceeded the speed limit:

| Excess of Speed Limit | Demerit Points |

|---|---|

| 0-15 | no demerit points (fine still applies) |

| 16-29 km/h | 3 points |

| 30-49 km/h | 4 points + 30-day suspension (G1/G2) |

| 40+ km/h on roads with a speed limit < 80km/h | 6 points + 30-day suspension (G1/G2) |

| 50+ km/h | 6 points + 30-day suspension (G1/G2) |

Potential Violations and Respective Demerit Points

While not an exhaustive list, here are some examples of how demerit points are applied:

Keep in mind that not all traffic tickets come with demerit points, but they may still affect your insurance rates.

How Demerit Points Affect Your Insurance

Insurers determine your rates based on a variety of factors, such as your age, gender, vehicle, location, commute distance, and claims history. While you can’t control some of these (i.e., demographic factors), you do have control over your driving risk.

Drivers with good driving habits are less likely to get into an accident and pose less risk to insurers. Because of this, they are more likely to get cheaper or preferred rates. Meanwhile, bad drivers can expect to be categorized as high-risk and have their premiums increase with every violation. Suspensions, which point to a track record of repeated violations, can raise your rates by thousands of dollars per year for three to five years.

However, it’s important to note that insurance companies don’t look at your demerit points. Rather, they look at convictions, which can include any traffic ticket — even minor ones that don’t accrue demerit points.

Some offences that don’t earn demerit points but may affect your insurance rates include:

- Driving without insurance

- Red light camera tickets

- Impaired driving/driving under the influence

Appealing Demerit Points

You have the right to dispute any ticket or traffic violation before the conviction goes on your record. If you’re successful, both the conviction and demerit points won’t be applied to your licence. “Convictions”, in this sense, are when:

- You’re found guilty in a court of law

- You pay for the ticket

Once you’re convicted, you can’t have the points removed from your record.

Key Advice From My Choice

- It’s in your best interest to drive safely and according to the law. Not only will this help you avoid getting demerit points, but it can also prevent costly accidents.

- Check your driving record at least once a year for your demerit points and convictions. Traffic officers aren’t required to advise you on how many points your offence has earned.

- If a conviction is inevitable, you can time the court hearing date after your insurance review or renewal to prevent it from affecting your rates.