Do Parking Lot Accidents Affect Insurance?

Yes, insurers treat parking lot accidents the same as any other type of accident. They use the same rules to determine who caused the accident, and if you are found to be at fault, it can affect your car insurance quotes.

What to Do After a Parking Lot Accident In Ontario?

Many people assume that, just because an accident occurs on private property rather than on a public road, you should react differently. However, parking lot accidents should be treated the same as any other car accident.

If you are involved in a parking lot accident, follow these steps:

- Check for injuries first. If anyone is hurt, call for medical help immediately.

- Assess the damage. If total damage appears to exceed about $5,000 in Ontario, the accident must be reported to a police Collision Reporting Centre.

- Exchange information with all drivers involved, including names, contact details, licence numbers, and insurance information.

- Take photos of the vehicles, damage, licence plates, and the surrounding area.

- Notify your insurance provider as soon as possible.

If you don’t report the parking lot accident, you can still receive a ticket after, and it won’t be as cheap as a parking ticket. Also, the other driver can still file a claim with their insurance company and determine that you were entirely or partially at fault for the accident, in this case your insurer may increase your rates without notice.

Who is At-fault in a Parking Lot Accident?

The cause of parking lot accidents is frequently misunderstood. Fault is determined on a case-by-case basis, just like in any other car accident. Due to the variety of factors at play, determining fault in a parking lot accident can be difficult.

Vehicles already travelling in a parking lot lane generally have the right-of-way over vehicles exiting a parking space. This is an important consideration when determining fault. In some cases, one driver is solely at fault, while in others, both drivers share blame.

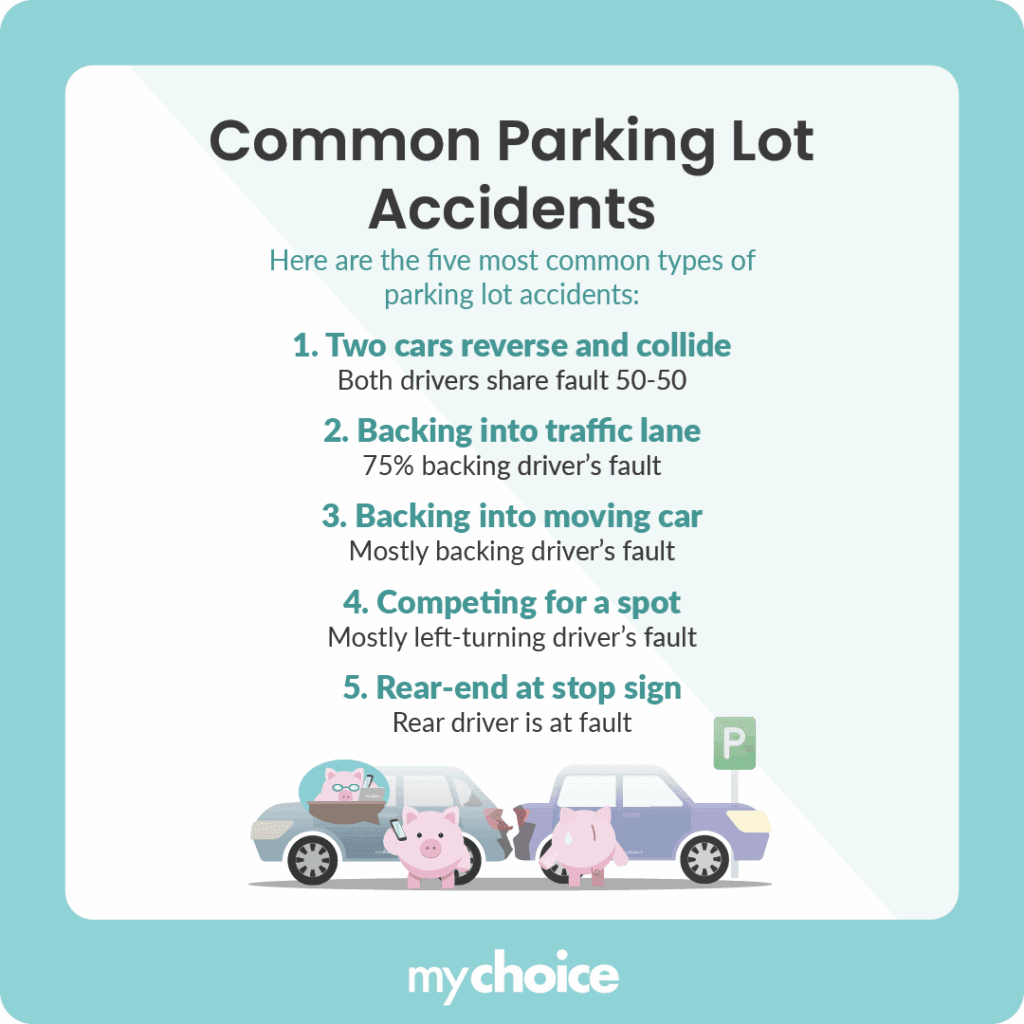

Common types of parking lot accidents?

The five most common types of parking lot accidents are:

Parking Lot Accidents: Hit & Run

A hit-and-run in a parking lot is terrible because if you can’t identify the driver, you’ll be responsible for the repair bill. Let’s analyze both situations.

Key Advice from MyChoice

- Always treat a parking lot accident like a regular collision. Exchange information, take photos, and notify your insurance company.

- Document everything at the scene. Photos, licence plates, and witness information can help determine fault and protect you if a claim is filed later.

- Consider getting collision coverage. It can help pay for repairs if the other driver leaves the scene and cannot be identified.