Critical illness insurance is worth it in Canada, depending on your financial situation, medical history, and whether or not you have dependents. While life insurance gives a payout to your dependents only upon your passing, critical illness pays out your benefit directly when you’re diagnosed with a specific, covered health issue.

It’s a supplementary type of insurance that provides for your loved ones so you can focus on recovering. However, it can also be too expensive for some people to get, especially those who are older or have pre-existing conditions.

Are you planning to get critical illness insurance? Keep reading to learn if you should purchase it, what it covers, and what may affect its cost.

Is Critical Illness Insurance Worth It?

Critical illness insurance can be a big help with expenses if you get diagnosed with an acute medical concern. In 2021, 45% of Canadians were found to be living with at least one major chronic disease. With the rising cost of health care, that’s a large chunk of the population that needs extra financial support – something that critical care illness can provide and help you prepare for.

However, critical illness insurance is not always the best solution for your financial situation or coverage needs. Here, we dive deeper into this insurance type’s pros and cons:

What Does Critical Illness Insurance Cover?

The specific medical conditions considered as “critical illnesses” vary from insurer to insurer, but these are the most common examples that are covered by Canadian providers:

- Different kinds of cancer, such as leukemia, lung cancer, and carcinomas may be considered critical illnesses

- Stroke, whether hemorrhagic or ischemic

- Paralysis, whether partial or total

- Dementia, including Alzheimer’s disease

- Heart attack

- Major organ failure on a waiting list

- Major organ transplant

- Permanent blindness in one or both eyes

Limitations and Exclusions in Critical Illness Insurance

Note that each illness covered by an insurer’s policy will be very carefully and specifically defined, and there may be specific requirements based on the severity of the condition. As a general rule, most insurers won’t provide coverage if:

- Your medical condition isn’t on its defined critical illnesses list, a.k.a. it’s a specified exclusion.

- You have a covered medical condition, but it existed or began before your policy’s effective date.

- It’s a less severe form of a covered condition.

Here’s a more in-depth explanation of these limits:

Should I Get Critical Illness Insurance?

Not sure if critical care insurance is right for you? If you fall under any one of these groups, you may consider getting this type of coverage as an extra safety net:

- Those with a family history of critical illness

- Individuals who want to supplement their health insurance

- People with a high risk of developing critical illnesses due to factors such as occupation and lifestyle choices

- Those looking for additional financial protection, especially for their dependents

There are other options you can look into if you feel that critical illness insurance doesn’t quite fit your needs. Here are other types of insurance that may help you and your loved ones if you get diagnosed with an acute medical condition:

- Whole or term life insurance

- Disability insurance

- Health insurance

Learn more about these different types of coverage by talking to your broker or insurance provider, or by reading our articles. Each provider has different conditions and coverage, so it’s essential to review policies carefully and shop around before purchasing one.

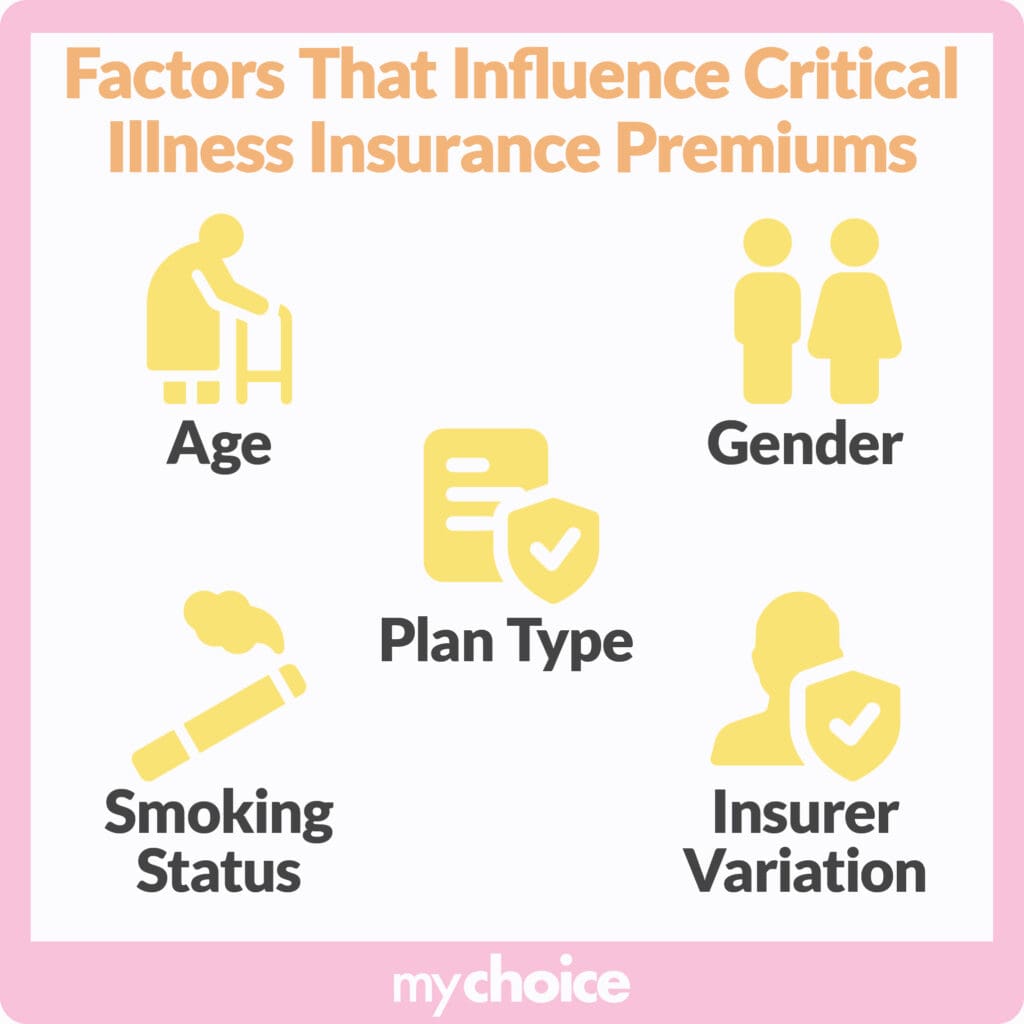

What Impacts the Cost of Your Critical Illness Insurance Premiums

The cost of your critical illness insurance premiums depends on several factors, such as your lifestyle and age. These are the most common considerations that may raise or lower your premiums:

- The amount of coverage: The higher the value of your policy and the more illnesses covered by your plan, the more expensive your critical insurance will be.

- Smoking and tobacco usage: Smokers, tobacco product users, and even those who use e-cigarettes a.k.a. vapes are generally charged higher premiums by health and life insurance companies. This is because they’re considered to be a high-risk group that’s more likely to develop certain diseases.

- Age: As with health and life insurance coverage, premiums go up with age because of the increased risk of developing critical diseases.

- Gender: Men and women are more susceptible to different illnesses, affecting their premium costs.

Key Advice From MyChoice

- Critical care insurance doesn’t cover all illnesses, so compare policies between providers to find the coverage that best suits your needs and preferences.

- This type of coverage provides financial security so you can focus on recovery and pay for medical expenses after you’re diagnosed.

- It’s common for companies to exclude covered critical illnesses if they began or existed before the policy’s effective date, so always check your policy’s terms and contact your provider if you have any questions.

- Shop around and compare rates using MyChoice until you find one that best suits your budget and preferred coverage.

- Consider getting critical care insurance to supplement an existing term or whole life insurance policy. Think of it as filling in the gaps to manage the financial impact of being diagnosed with a serious illness, which often isn’t covered by life insurance.