It’s frustrating to get denied life insurance coverage for whatever reason, especially if you need the protection. Fortunately, that isn’t the end of the road. You can get life insurance after being denied coverage by asking for a reassessment, reapplying, or applying for alternative life insurance policies.

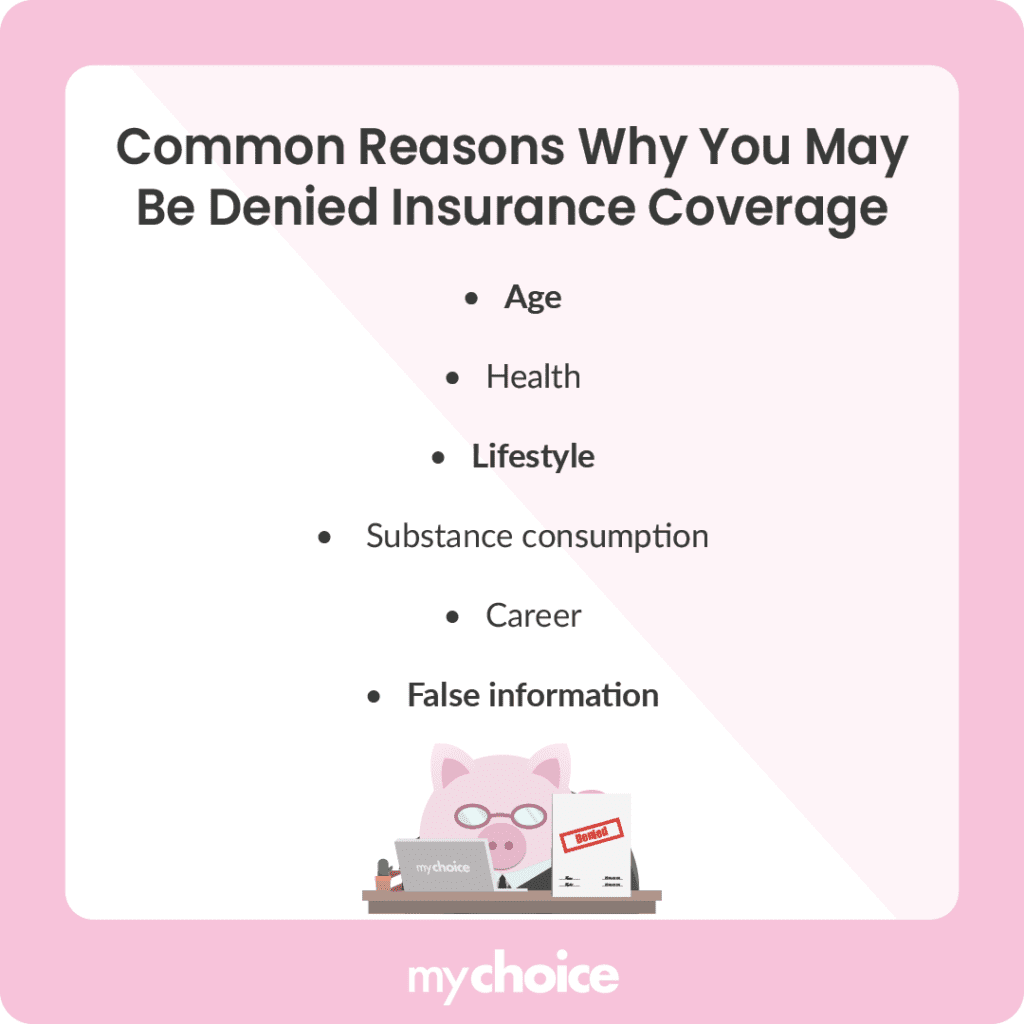

Why You May Be Denied Insurance Coverage

Life insurance companies generally deny your life insurance coverage because you’re deemed too risky to insure. Here are some common reasons why life insurance companies turn your application down:

What To Do After Getting Your Life Insurance Coverage Denied

Even if you expect to get your life insurance application approved, being prepared is never a bad idea. Here’s a step-by-step guide of what to do after your application gets denied to ensure you know what to do next.

1. Find Out Why

If you don’t know why your application was denied, any future attempts at applying may end up similarly. The best first step is to ask the insurance company why your application was declined. They’ll generally provide further details on the reasons for your denial.

If necessary, verify the information from the insurance company. For instance, if their medical examination reveals a health issue you didn’t realize you have, double-check with your doctor to ensure you really have that condition. You can also ask for your submitted information from the MIB Group (formerly the Medical Information Bureau) to verify that everything you submitted was truthful.

2. Get a Second Opinion

The insurance company that rejected you isn’t the only fish in the sea. Try applying to different life insurance companies and see if they can grant you coverage. You can also use MyChoice to compare quotes from various insurance providers to find the best deals.

If you can get insurance coverage with one of the other insurance companies, that’s good. But if you’re still denied or want coverage with the first company, move on to the next step.

3. Appeal the Decision

Sometimes, genuine mistakes happen on your end or the insurance company’s. If you think either party made an honest mistake, ask for a reassessment. Verify the information you submitted and ensure you get everything right.

4. Try Reapplying Later

If your application was rejected for valid reasons, but you still insist on getting a policy from that insurance company, you can consider reapplying. If you’re rejected due to issues that can be controlled, like a smoking habit, wait until the problem is more under control before reapplying for that policy.

5. Consider Alternatives

If you still can’t get a policy after reapplying, it may be time to consider other options. You can either try to get the same type of policy with exclusions or find other policies that have more lenient qualification requirements.

Backup Plans: Alternative Life Insurance Coverage Options

You still have alternatives if the usual term or whole life insurance policies don’t work out. Let’s take a look at some of the available alternative options for life insurance coverage if your application gets denied.

Key Advice From MyChoice

- If you get denied life insurance coverage, you can appeal the decision or reapply later. If both methods fail, consider looking for other insurance companies or alternative policy types.

- Work with insurance advisors or use MyChoice to compare life insurance quotes from various insurance providers to find the best company for you.

- Available alternatives that you can apply for include guaranteed life insurance, group life insurance, and mortgage life insurance. Choose from these depending on your lifestyle, age, and financial obligations.