If you have an older car that you don’t drive around much, you might wonder whether collision coverage is still necessary. After all, if your car is constantly parked in a garage or storage, what is there to protect it from?

Get all the answers you need regarding whether to stop or continue collision coverage in this comprehensive guide.

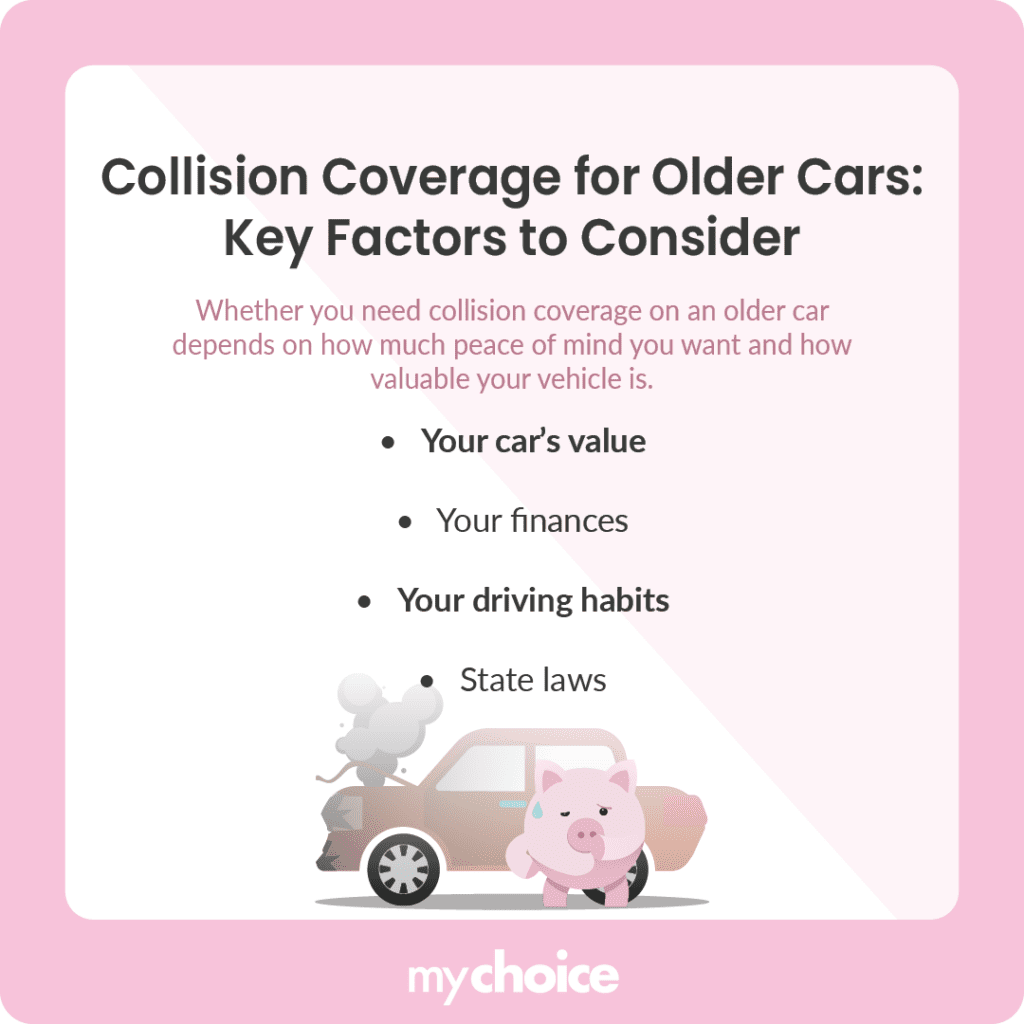

Do You Need Collision Coverage on an Older Car?

Whether you need collision coverage on an older car depends on how much peace of mind you want and how valuable your vehicle is. You can make an informed decision about collision coverage for your older vehicle by considering these factors:

When to Stop Collision Coverage

While collision coverage can give you peace of mind, especially if you live in an accident-prone area, dropping it sometimes makes more sense than maintaining it. Besides your vehicle being low-value, other instances in which you might consider dropping collision coverage include the following:

Computing Your Vehicle’s Value

So, you’re torn between keeping your collision coverage and dropping it, which involves calculating your vehicle’s value. Where do you start?

You can use an online valuation tool to get an estimate on older or certified pre-owned vehicles. These resources allow you to find your vehicle’s make and model and get a quote, but they may not be the most accurate way to value your car.

Another option is consulting your local dealership. If you’re still in touch with the dealership that sold you the car, you can ask them to value your vehicle based on a physical inspection and against current market conditions. It’s best to provide as much information about your car, such as its repair history and maintenance reports.

Helpful information to have on hand when you get your vehicle valued includes the following:

- The car’s make and model

- The car’s mileage

- The overall condition of the car, including its exterior, interior, and mechanical components

- Additional features like leather seats, a sunroof, a navigation system, or a sound system

Alternatives to Collision Coverage

Consider these alternatives if you’re dropping collision coverage on your old car.

Key Advice From MyChoice

- Keep as many documents and as much information on your older car as possible, especially if you plan to stop collision coverage. Tracking the car’s history and condition can tell you whether keeping the policy is worth it.

- Evaluate your financial situation and determine whether paying for peace of mind is worth it. Consider financial obligations like debt and other home-related expenses.

- Review your insurance policies regularly and keep insurance records. You might find better options for an older vehicle.