Renewing your home insurance policy may seem like a routine task until you notice your rates have increased. As a Canadian homeowner, you might wonder why your rates have increased and if the rise is justified.

Home insurance rates don’t stay static, and there are reasons why they might increase upon renewal. But understanding why your premiums rise and what you can do about it can empower you to keep your rates at a reasonable price and potentially save money.

Recent Trends in Canadian Home Insurance Rates

Home insurance rates in Canada spiked by 7.66% in 2024, with the highest provincial spikes in Saskatchewan and Manitoba.

According to the Insurance Bureau of Canada’s (IBC) policy development manager Cecilia Omole, “The data reveals that a series of contributing factors – namely, the growing cost of rebuilding and repairing damaged property and the increasing frequency and severity of natural catastrophes – are driving up the cost of home insurance.”

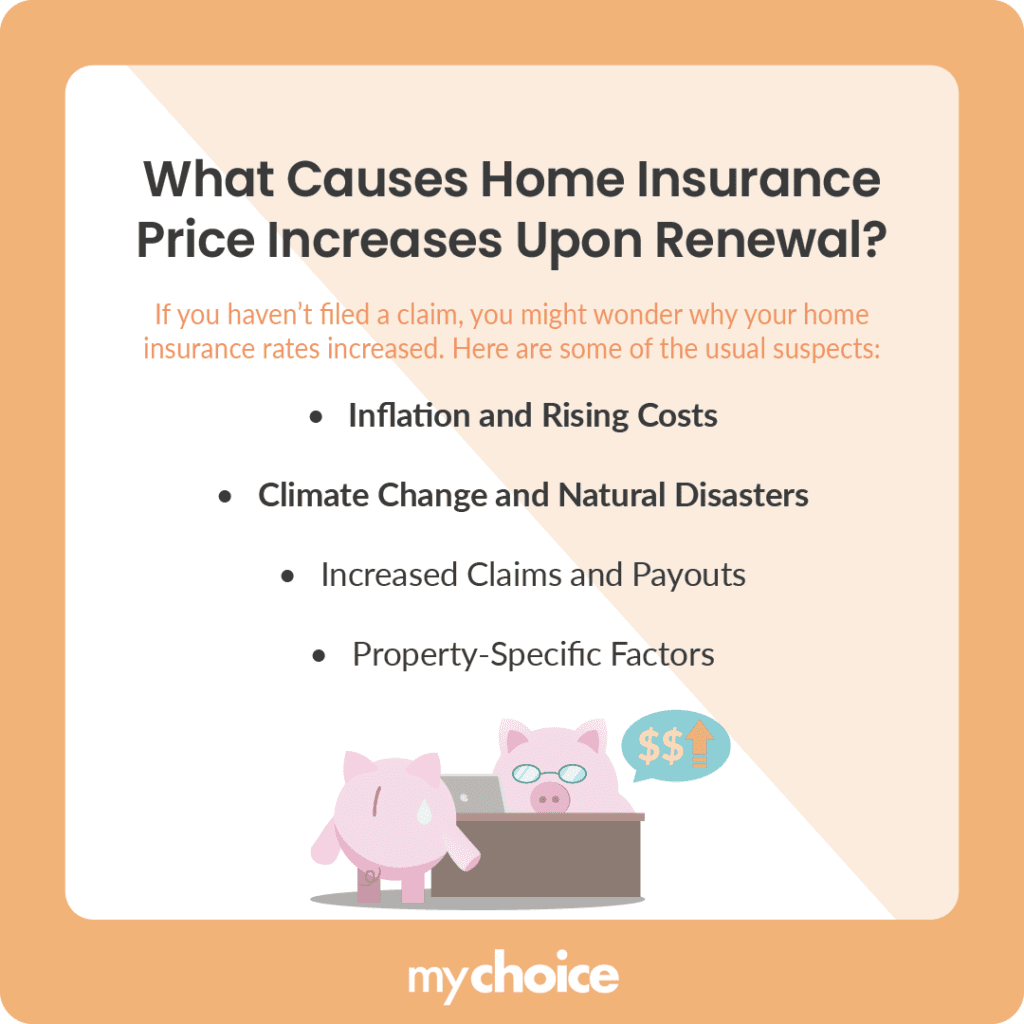

What Causes Home Insurance Prices to Increase Upon Renewal?

If you haven’t made a claim on your policy, you may wonder why your home insurance rates have gone up. Here are some of the usual suspects.

Tips for Managing and Reducing Home Insurance Premiums

Sometimes, insurance increases are inevitable, especially with growing inflation and a struggling economy. Still, there are some ways to keep your premiums low and manageable.

Key Advice from MyChoice

- Keeping up with inflation and economic changes can provide a perspective on how your home insurance rates might change.

- If you can pay for minor repairs and replacements out of pocket, do so. It may end up costing you more in the long run if you make several minor claims.

- Protect your home from environmental risks like storms, snow, vandals, and thieves by installing reliable security systems and weatherproof materials.